There is a possibility of error at each data processing stage, including downloading, uploading, validating file consistency, and record matching. You may, for instance, download or upload an obsolete file or reconcile the wrong accounts. Consequently, you may overestimate your cash flow and increase the cost of future adjustments. It allows businesses to identify and address issues caused by bank fees and taxes, ensuring the balance sheet reflects the correct financial status. During the reconciliation process, corrections may be made to the general ledger with adjusting journal entries.

Compare the Balances

The information provided in this article does not constitute accounting, legal or financial advice and is for general informational purposes only. Please contact an accountant, attorney, or financial advisor to obtain advice with respect to your business. An investigation may determine that the company wrote a check for $20,000, which still needs to clear the bank.

- If you decide to hire someone to help, make sure they are following GAAP, or have credentials and experience that you trust.

- Accounting software is one of a number of tools that organizations use to carry out this process thus eliminating errors and therefore making accurate decisions based on the financial information.

- The charges have already been recorded by the bank, but the company does not know about them until the bank statement has been received.

- Examine the source papers for any changes between approval and transaction completion, especially if they are paper-based.

- This is a bit like carrying out a personal accounting reconciliation using credit card receipts and a statement.

Streamlining Travel and Expense Management

For example, the internal record of cash receipts and disbursements can be compared to the bank statement to see if the records agree with each other. The process of reconciliation confirms that the amount leaving the account is spent properly and that the two are balanced at the end of the accounting period. Reconciliation holds significant importance in accounting due to several reasons. Firstly, it helps in detecting errors and discrepancies, ensuring the accuracy and integrity of financial information.

Suspense Account Reconciliation

Accounting software is like a database for all of your business’s financial transactions. It helps you follow basic accounting principles so that you can keep your books up to date and in order, which is especially important come tax season. Most software uses double-entry accounting, meaning it factors in assets, liabilities and equity, in addition to revenue and expenses. Verify that all purchase transactions are authorized and processed correctly. Ensure that amounts recorded by the Accounts Payable ledger match the bank statement history for the amounts paid.

Another advantage of reconciliation is that it can aid in preventing or uncovering fraud, embezzlement, and other unethical activities. While some scammers are terrible geniuses at covering their traces, most offenders are not quite as intelligent. Careful attention to detail and evaluation of account reconciliations by a third party can aid in the detection of many cases of fraud. Mark any cash book transactions corresponding to similar transactions on the bank statement. Keep track of all transactions in the bank statement; any proof, such as a payment receipt, do not back them. The process of resolving inconsistencies between two sets of records by shifting the amount in question to a suspense account is called suspense account reconciliation.

Look for Transactions That Appear in Both the Cash Book and the Bank Statement in Reconciliations

The same plans help speed up the inventory count process by allowing businesses to use mobile devices as barcode scanners. And unlike some competitors that only track single inventory items, QuickBooks Enterprise lets you track inventory parts plus assemblies. You can also track the cost of goods sold and adjust inventory for loss or shrinkage. Reporting capabilities increase with each plan, but even the least expensive Simple Start plan includes more than 50 reports.

It provides an opportunity to record their cash position and forecast their cash flow with a higher degree of accuracy. And while most financial institutions do not hold you responsible for fraudulent activity on your account, you may never know about that fraudulent activity https://www.wave-accounting.net/ if you don’t reconcile those accounts. Regular account reconciliation should be combined with invoice reconciliation as part of your internal controls in accounts payable. For a small business or an account with very few transactions, reconciliation may not be a challenge.

Accounting software automation and adding a procure-to-pay software, like Planergy, can streamline the process and increase functionality by automatically accessing the appropriate financial records. Keeping your accounts reconciled is the best way to make sure that your balances are accurate and an important part of ensuring adequate financial controls are in place. While the reconciliation process remains the same, with two sets of documents compared for accuracy, the difference lies in what is being reconciled. As CEO and Co-Founder, Mike leads FloQast’s corporate vision, strategy and execution.

Secondly, reconciliation plays a crucial role in identifying and preventing financial fraud, and safeguarding the business’s financial health. Lastly, it enables businesses to perform effective financial analysis, aiding decision-making processes. Delays in vendor reconciliation can affect cash flow management and strain vendor relationships. Nanonets automates the reconciliation process, ensuring that it is completed promptly.

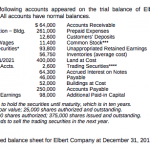

Companies need to reconcile their accounts to prevent balance sheet errors, check for possible fraud, and avoid adverse opinions from auditors. Companies generally perform balance sheet reconciliations each month, after the books are closed for the prior month. This type of account reconciliation involves reviewing all balance sheet accounts to make sure that transactions were appropriately booked into the correct general ledger account. It may be necessary to adjust some journal entries if they were booked incorrectly. This type of reconciliation is used by businesses to reconcile the balances of bills and invoices of customers, which are yet to be paid by the customers and hence yet to be received by the business. These bills and invoices are matched to the individual balances owed by each customer against each invoice and then the overall balance of accounts receivable.

Businesses maintain a cash book to record both bank transactions as well as cash transactions. The cash column in the cash book shows the available cash while the bank column shows the cash at the bank. Once the balances are equal, businesses need to prepare journal entries for the adjustments to the balance per books. All of these things will occur at some point in the life of any organization. However, if you reconcile your accounts regularly, you may avoid errors as they happen.

The company’s current revenue is $9 million, which is way too low compared to the company’s projection. For example, a company may review its receipts to identify any discrepancies. While scrutinizing the records, the company finds that the rental expenses for its premises were double-charged.

Reconciliation is typically done at regular intervals, such as monthly or quarterly, as part of normal accounting procedures. Account reconciliation is a vital process that helps businesses maintain their financial health by identifying errors, preventing fraud, and ensuring the validity and accuracy of all financial statements. Reconciliation ensures that accounting records are accurate, by detecting bookkeeping errors and fraudulent transactions.

Reconciling these accounts is usually a simple matter of making sure that the balance in the relevant subledger or schedule matches the balance in the general ledger. Since 2006, when Sarbanes-Oxley became effective, public companies have been required to have internal https://www.accountingcoaching.online/is-accumulated-depreciation-an-asset-or-liability/ controls that are adequate to prevent material misstatement. Performing regular balance sheet account reconciliations and reviewing those reconciliations is one form of internal control. Auditors will always include reconciliation reports as part of their PBC requests.

These steps can vary depending on what accounts you are reconciling, but the underlying premise is always the same – compare your ending balance against supporting documentation and make any adjustments as needed. Account reconciliation is a financial reconciliation, with no real difference, except for how the results of the reconciliation process will be used. Larger businesses with several branches may also need to complete intercompany reconciliations. explicit and implicit costs and accounting and economic profit Depending on your business, you may also want to reconcile your inventory account, which is typically completed by doing a complete accounting of all inventory on hand. A profit and loss statement, also known as an income statement summarizes revenue and expenses that have been incurred during a specific period. Balance sheets and profit and loss statements are both essential resources for determining the financial health of your business.